As government and business leaders gather in Dubai for the latest round of climate talks, how to accelerate the growth in renewable energy is a core theme of the meeting. Enabling clean energy technologies to grow at the pace and scale needed to meet global climate targets, however, will ultimately depend on the rate at which the critical mineral resources needed to build them can be found and mined.

Under the conditions outlined in the International Energy Agency’s net zero emissions by 2050 scenario, critical minerals supply will need to grow by three and a half times by 2030 to meet energy demands. The proposal under consideration at COP28 to triple global renewable energy capacity by 2030 would place even greater pressure on critical mineral global supply chains.

However, new critical minerals mining projects can take up to 20 years to be developed as project timelines are routinely beset by delays. If the average time to production does not reduce to between 5 and 10 years, there is a risk that a critical minerals shortage before 2030 could cause the global 2050 net zero emissions target to be missed.

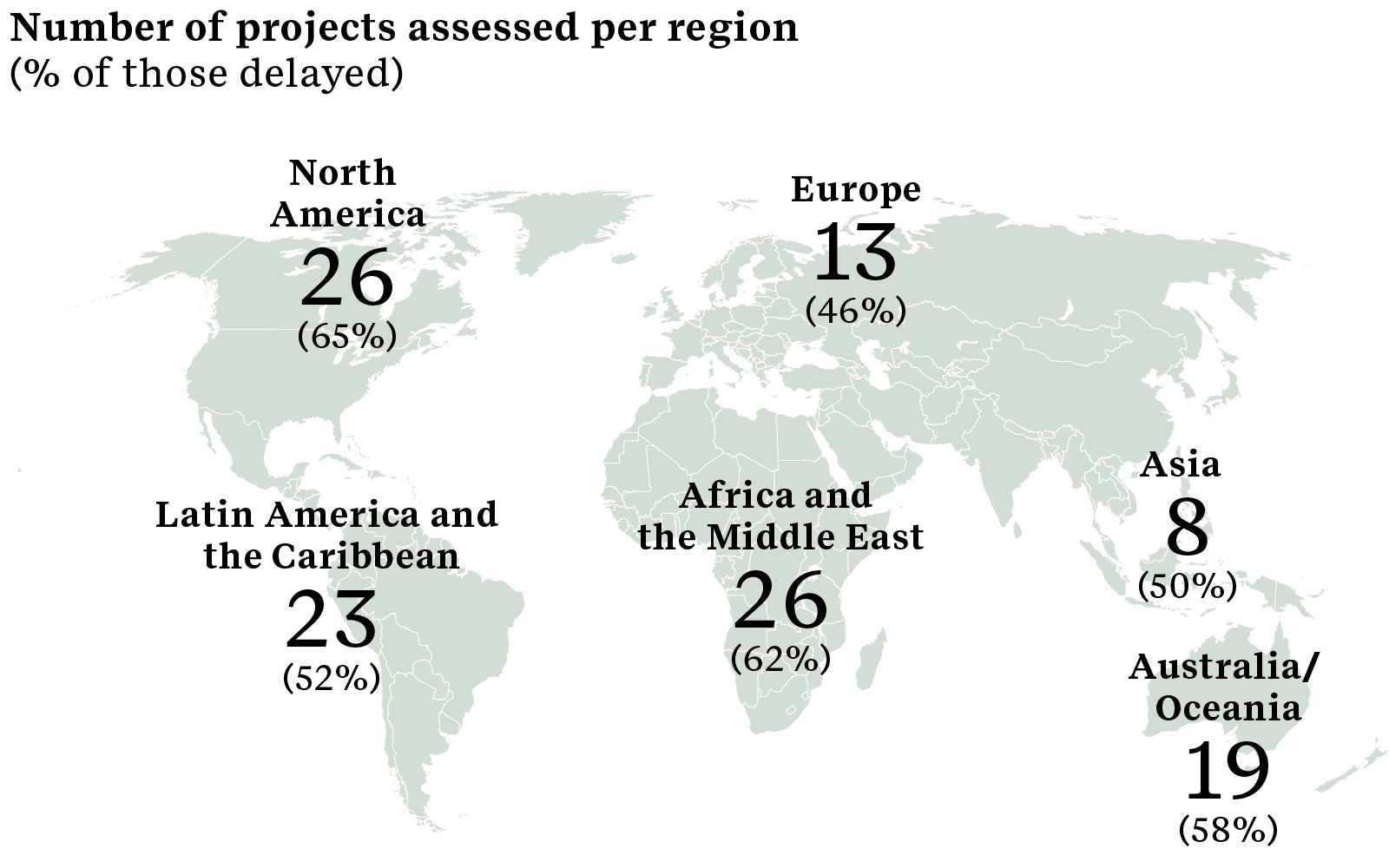

ERM analysis of more than 100 global critical minerals projects—mining primarily cobalt, copper, graphite, lithium, manganese, nickel, rare earths, lanthanides or zinc— shows that between 2017 and 2023 almost 60% of projects reported pre-production delays ranging from a few months to several years.

Source: ERM analysis (2017-2023 data)

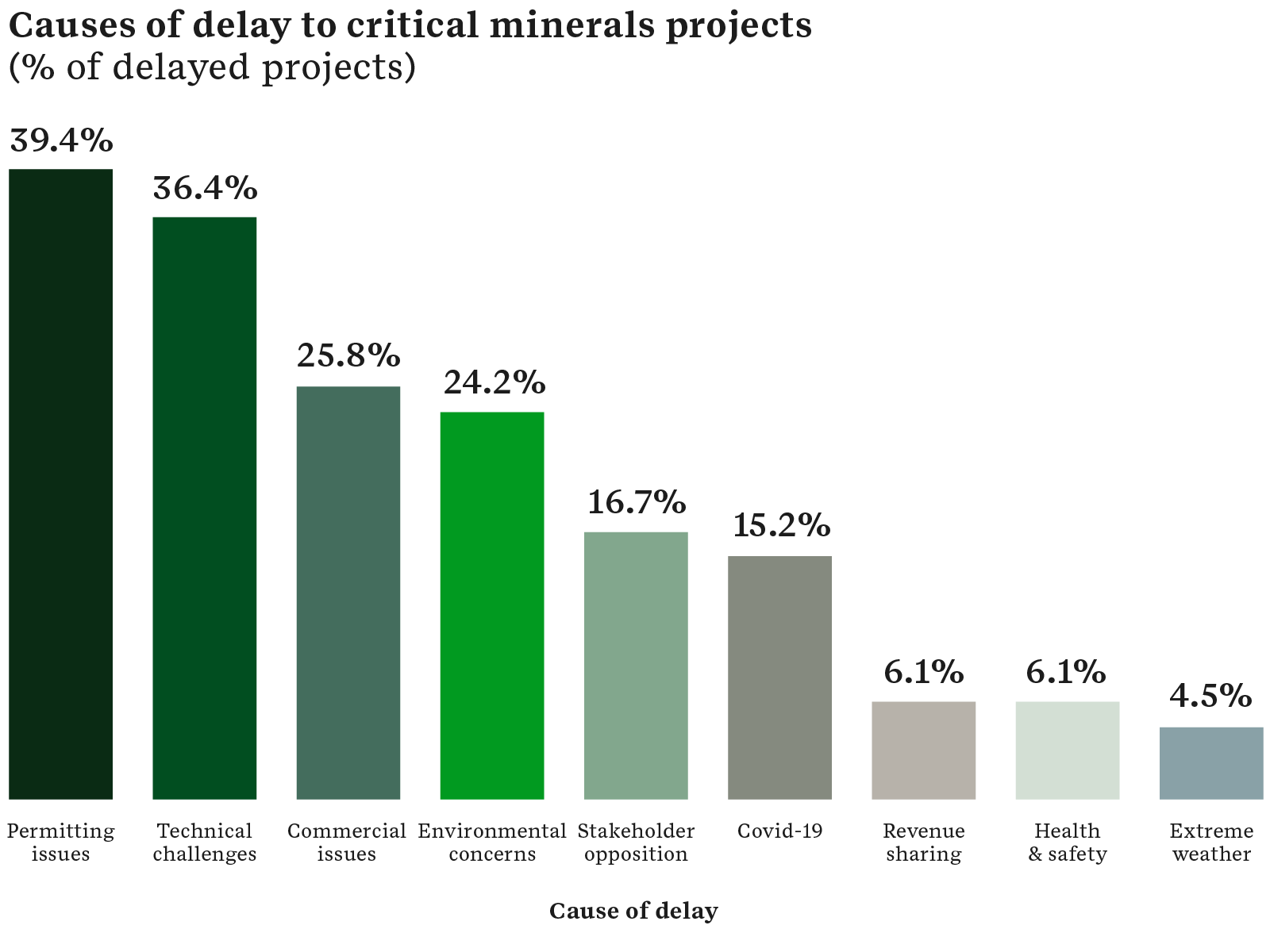

The three biggest causes of delay to critical mineral mine development are permitting issues (39%), technical challenges (36%), and commercial issues (26%). Sustainability issues, particularly environmental concerns (24%) and stakeholder opposition (17%), were found to have contributed significantly to these top three delays.

The financial implications of these delays are significant. ERM research shows that a mining project with capital expenditure of between US$3–5bn will suffer roughly US$20m per week in terms of net present value from delayed production.

Source: ERM research (2017-2023 data)

In order to increase the pace and scale of critical minerals mine development, three core challenges and interventions will be key:

Challenge 1: Building stakeholder trust in the mining industry

Despite the emergence of more than 20 mining sustainability standards over the past two decades, alongside state, federal and regional jurisdictional requirements designed to improve environmental and social performance, stakeholder trust in the sector remains low. According to a 2022 poll commissioned by the International Council on Metals and Mining (ICMM), the mining sector has the lowest level of public trust compared to any other industry, below oil and gas.

Our research found that 62% of the projects delayed by permitting issues were due to stakeholder opposition or concerns around the project’s environmental impacts (with the remainder largely the result of regulatory constraints). In many cases, stakeholder concerns around the mine’s impact on the environment were not factored into the project’s design, with companies instead focused on proving the resource in isolation of ESG factors or stakeholder engagement. This has the potential to hold up public consultations and, in some cases, require a re-design of the project, resulting in further delays and costs for the operator.

Defining what good looks like

The entire critical minerals value chain would benefit from supporting project developers to improve their approach to environmental and social issues, whilst recognising that competing ESG standards, although well intentioned, can create prohibitive financial burden and confusion amongst many companies.

The confusion regarding standards has been further complicated by the increasing intervention of downstream customers in upstream activities. Notably, original equipment manufacturers (OEMs) are becoming more active in the earlier stages of the mining lifecycle, securing long-term offtake agreements or in some cases taking minority stakes in critical minerals projects. An example of this is Stellantis, an automotive manufacturer, taking minority stakes in lithium and copper projects in Argentina in February this year. While involvement from OEMs creates a vital source of investment, it can bring with it new complexities for project developers, who may have to navigate competing ESG standards from the OEMs and other downstream customers.

The wider value chain, including end users, OEMs and investors, can play a vital role in supporting upstream development of critical minerals projects by working together to align on goals, implementation, de-risking considerations and even efforts to cover additional upfront costs. This includes consolidating ESG standards or enabling a pathway for acceptable equivalency across the 20+ standards that currently exist.

Building stakeholder trust is a complex and long-term undertaking that also requires a commitment to greater transparency. It will be important for mining companies to share candidly the lessons learned from previous experience and demonstrate how mining has improved its effectiveness in managing environmental and social impacts. Recognizing where performance fell short and sparked remedial action can help build better stakeholder relationships. If this is sustained over the long term, trust may start to be repaired.

Challenge 2: Avoiding delays early in the project’s development

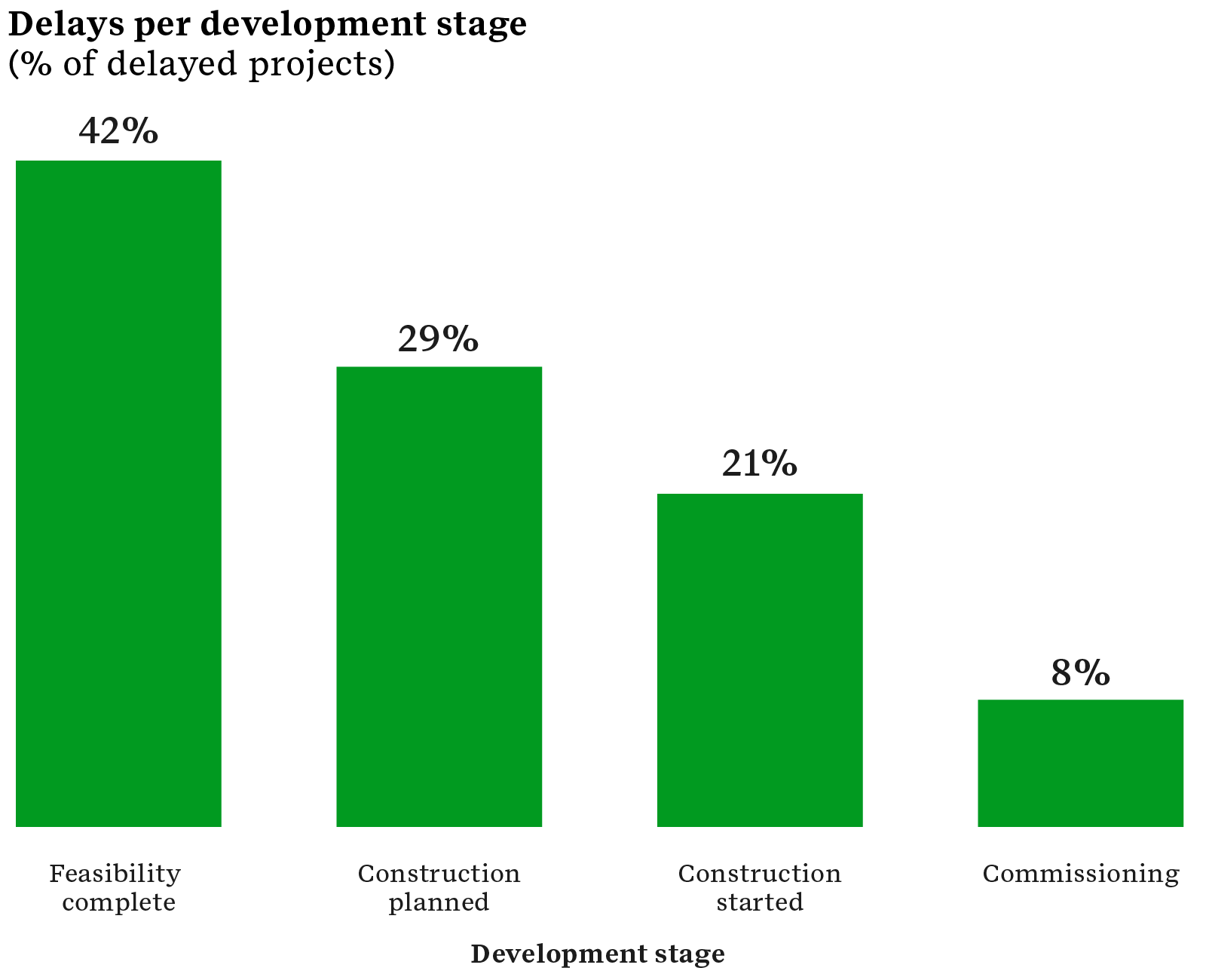

ERM research shows that over 40% of delays to critical minerals mining projects occur early on, at the feasibility stage, with the rate of delay then falling as the project develops. Crucially it is at the feasibility stage that stakeholders outside of the industry (and those most likely to voice opposition) become aware of the project’s existence and investors begin to commit capital to studies assessing the project’s viability and to secure key approvals.

Source: ERM analysis (2017-2023 data)

Most stakeholder interest and/or opposition tends to be driven by a debate around the environmental and social impacts of a mining project, though discussions around revenue sharing (beyond direct employment or ‘hand outs’) are increasingly common. This is a crucial point at which companies need to create a shared value proposition in collaboration with stakeholders, providing clarity and transparency, listening to concerns and dispelling misinformation and misperception. The tone in any debate of this nature is often set early on and can influence stakeholder perceptions well into the production stage of a project.

This reality currently counts against many of the junior mining companies that dominate the development of critical minerals mines. Because they are typically looking to sell their asset to a mid-cap or major or want to avoid unnecessarily raising expectations before the resource has been proven, they often prefer to keep a low-profile. This misses an opportunity to proactively engage stakeholders and get input into what the modern mine could look like and how environmental impacts can be avoided or managed.

Getting ESG issues right early on

De-risking feasibility stage projects will be crucial to the smooth and efficient progression of mining projects. To prevent permitting delays or stakeholder opposition, developers need to work to decouple projects from stakeholders’ negative preconceptions of mining by taking the time to build trust early through open and equal dialogue.

ERM’s sustainability model for mining, ‘The Mine We All Want to See’, outlines a more forward-looking approach for miners, based on hard wiring positive environmental and social outcomes, defined through stakeholder collaboration, into project design from inception:

Source: ERM

ERM has worked with several critical minerals miners to de-risk projects by incorporating more rigorous environmental and social standards into the design and concept of their mines.

Challenge 3: Understanding local social, political, environmental and regulatory risks

Reflecting the scope and range of global geopolitical, regulatory, social and environmental dynamics across geographies, ERM research shows that the location of critical minerals projects can also heavily influence the risk of delays, stakeholder challenges and higher costs.

For example, mining projects located in environmentally sensitive jurisdictions come with additional expectations for mining companies to manage their environmental impacts and tackle stakeholder challenges. According to research by S&P Global Sustainable, 1,200 mining sites worldwide are in key biodiversity areas (with 29% of these projects involving critical minerals).

In Latin America, delays were driven markedly by difficulties in obtaining the necessary permits (67% of delayed projects in the region). ERM’s experience of working with mining projects across this region has shown significant capacity constraints in many regulatory agencies handling permitting.

National politics also impact permitting delays. In Mexico, hundreds of mining projects have been suspended as the government looks to take a tougher line on environmental permitting and take a greater stake in the lithium sector.

In Africa, 44% of the projects delayed were related to government efforts to renegotiate mining licenses. Contract renegotiations and fiscal disputes in Tanzania and the DRC were central drivers of this.

Understanding the local context

Mining companies, investors, OEMs and other players upstream of the critical minerals value chain need to have a strong understanding of the unique environmental, social, regulatory and political context in which they operate, to avoid making missteps that could have a lasting impact on a mining project’s development.

Junior miners are commonly managed out of one jurisdiction (often listed on the stock exchange of that country) but explore and seek to develop projects in a different jurisdiction, often with higher social, political or regulatory risk, where they can struggle to understand or meet local expectations. For example, there are currently nearly 40 Australian Securities Exchange-listed juniors exploring in Quebec, needing to navigate potential issues around legislation, language barriers and consultation with First Nations to gain consent. Similarly, for diversified majors, a singular corporate strategy will not necessarily account for local jurisdictional and community expectations. By focusing on rigorous due diligence and design, a mine project can be developed in a way that incorporates local stakeholder priorities and concerns.

Policy, capacity and capability is also lacking amongst regulators in hot spots of critical mineral investment. Policymakers need to take on the role of enablers by supporting the development of shared infrastructure for critical minerals projects and building the ecosystem necessary to enable projects. Canada, for example, has taken a bold step with its US$1.5bn Critical Minerals Infrastructure Fund, aimed at boosting critical mineral project economics, enhancing feasibility, improving access to remote regions, and positioning Canada as a major processor, refiner, and producer of advanced chemicals. This initiative is set to catalyse infrastructure development for lithium projects in northern Quebec and Manitoba through road and rail upgrades, with potential benefits extending to exploration campaigns for nickel and cobalt in Ontario through improved power grid connections.

Similarly, the Australian government has doubled the amount of money on offer to support critical minerals projects. The funding boost of an additional US$1.3b will increase the capacity of Australia’s Critical Minerals Facility to finance mining and processing projects for materials. The initiatives of Canada, Australia and other countries, pale in comparison to the US Inflation Reduction Act, which is creating a transformative investment opportunity across the critical minerals value chain.

Accelerating the transition

The urgency of the clean energy transition is already placing increasing and sustained pressure on miners to develop mining projects at scale and pace. This will ramp up even further over the next 10 to 20 years, as efforts redouble to develop clean energy technologies capable of meeting stringent global emissions and sustainability targets.

While our research shows that the obstacles to meeting this demand are extensive, an approach that focuses on early preparation, thorough engagement and consultation, and raising environmental and social standards can create a critical minerals industry that is fit for future growth.

This is the first phase of a study that ERM is undertaking to better understand the global implications of the bottleneck at the beginning of the critical mineral value chain. The second phase of this study, incorporating perspectives of stakeholders across and around the critical minerals value chain, will be released in 2024.

Many thanks to Jennifer Ukachukwu Amarachi and Triv Naidoo for contributing to this ERM research.

Contacts:

Toby Whincup, Critical Minerals Director

Toby.Whincup@erm.com

Charles Pembroke, Associate Partner

Charles.Pembroke@erm.com